Executive Summary

To begin with, the global memory market in early 2026 is entering a gradual recovery phase following the significant supply corrections seen during the previous cycle.

Several industry indicators help illustrate the current market situation:

NAND module prices increased approximately 3–8% month-over-month in February, while upstream wafer prices showed higher volatility.

DRAM spot prices remained relatively stable, typically fluctuating within a 3–5% range in the short term.

Enterprise SSD demand is estimated to be growing around 15–20% year-over-year.

Global PC shipment growth for 2026 is currently forecast at 3–5% according to industry analysts.

These indicators suggest that the memory market is moving into a controlled recovery phase. Major manufacturers continue to maintain disciplined production strategies while enterprise infrastructure demand—particularly from cloud and AI workloads—keeps expanding.

Based on current supply discipline and enterprise demand momentum, moderate upward pricing pressure is expected to continue through Q4 2026, although the pace of price increases may stabilize compared with the sharp recovery seen earlier in the cycle.

NAND Flash Market Update

Demand Structure Shift: AI Infrastructure and Enterprise Storage Expansion

First of all, the NAND industry remains highly concentrated. The top five manufacturers account for more than 90% of global NAND supply, giving leading vendors significant influence over production strategies and market pricing.

Major suppliers include:

While production discipline remains an important factor in the current market recovery, the most significant structural change in recent years has been the rapid expansion of AI-driven infrastructure demand.

The global deployment of AI computing clusters, large-scale model training environments, and inference platforms has dramatically increased storage requirements within hyperscale data centers. These workloads require vast amounts of high-performance SSD storage for datasets, model checkpoints, and high-speed data pipelines.

Industry estimates indicate that AI-related storage demand is growing at more than 30% annually, making it one of the fastest-growing segments in the memory ecosystem.

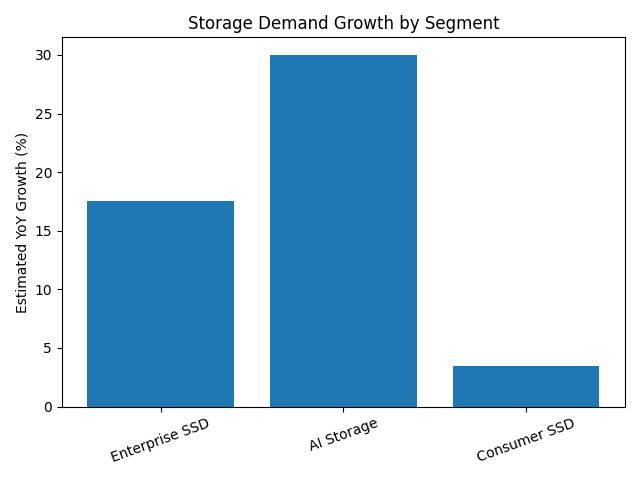

As a result, enterprise storage demand has significantly outpaced the consumer segment. Recent shipment trends suggest:

Enterprise SSD demand growth: approximately 15–20% YoY

AI server infrastructure demand: growing 30%+ YoY

Consumer SSD demand: expanding only 2–5% YoY

At the same time, NAND manufacturers have remained cautious about expanding production capacity. After experiencing the severe oversupply cycle during 2022–2023, most vendors continue to prioritize capital discipline and controlled capacity utilization rather than aggressive production expansion.

Consequently, a larger portion of available NAND supply is increasingly allocated toward enterprise SSDs and data-center storage systems, which typically provide higher margins and long-term supply contracts.

This shift has important implications for the broader storage market. Even when consumer demand remains relatively stable, the growing allocation toward enterprise infrastructure can tighten supply for client SSDs.

Therefore, the recent price recovery in consumer SSDs is not solely the result of production cuts. Instead, it reflects a broader structural reallocation of NAND supply toward AI infrastructure and enterprise storage applications.

NAND Price Trend Overview

In addition to structural demand changes, NAND pricing has entered a clear recovery phase during the past several quarters.

However, price dynamics vary across different levels of the supply chain. Upstream wafer pricing tends to respond more quickly to supply adjustments, while downstream storage products reflect these changes more gradually.

Recent market observations indicate the following pricing trends:

NAND wafer prices: increased approximately 20–40% quarter-over-quarter during the recent recovery cycle

SSD module prices: increased approximately 30–40% QoQ as component costs gradually passed through the supply chain

DRAM prices: experienced stronger recovery momentum, rising roughly 30–50% QoQ in certain segments

This pricing recovery reflects the combined effects of production discipline, improved demand conditions, and the rapid expansion of enterprise storage requirements driven by AI infrastructure.

Looking ahead, the pace of price increases is expected to moderate compared with the sharp rebound seen earlier in the cycle.

Current industry projections suggest:

Q2 2026: NAND prices may continue rising around 10–20%, depending on contract negotiations and enterprise demand strength

Q3 2026: pricing trends will likely depend on inventory levels and the pace of enterprise infrastructure deployment

DRAM and DDR Market Update

DDR4 Phase-Out Cycle

Turning to the DRAM market, one major structural shift is the gradual phase-out of DDR4 production.

Industry capacity allocation has changed significantly in recent years:

As manufacturers transition production lines to DDR5, certain DDR4 capacities have become tighter. This supply adjustment occasionally leads to short-term price fluctuations of around 5–10% per month for specific DDR4 configurations.

In many cases, products approaching the end of their lifecycle tend to experience structural pricing volatility as production capacity declines.

DDR5 Adoption Growth

Meanwhile, DDR5 continues to gain momentum across both consumer and enterprise platforms.

Recent adoption data shows:

New PC platform DDR5 adoption: above 70%

Server DDR5 penetration: above 80%

High-density DRAM modules (32GB+) demand: growing more than 20% YoY

The shift toward DDR5 is driven by the need for higher bandwidth and improved memory efficiency in modern computing systems, especially for AI workloads and high-performance servers.

Short-Term DRAM Pricing Outlook

In terms of pricing trends, DRAM market volatility remains relatively moderate compared with previous cycles.

Current indicators suggest:

Overall, the structural migration toward DDR5 is gradually reducing the risk of long-term oversupply in the DRAM market.

Key Market Indicators to Watch

To better understand future market movement, several key variables should be monitored closely.

Inventory Levels

First, inventory cycles across the memory industry have improved significantly.

Lower inventory levels increase price elasticity, meaning prices can respond more quickly to demand changes.

AI Server Demand

Second, AI server deployment is becoming a major driver of memory consumption.

Key metrics include:

These systems require both high-capacity DRAM and large-scale SSD storage, increasing demand across the entire memory ecosystem.

PC Shipment Growth

Third, the consumer PC market is expected to remain stable but not explosive.

Industry data suggests:

This moderate growth indicates that consumer memory demand will expand gradually rather than rapidly.

Q2–Q3 2026 Price Forecast

Based on current supply discipline, enterprise demand growth, and improving inventory conditions, the memory market is expected to remain in a recovery phase through mid-2026, although the pace of price increases may gradually moderate.

SSD Price Outlook

For NAND-based storage products, the strongest price recovery occurred during the early stage of the market rebound. Moving forward, price increases are expected to continue but at a slower pace.

Industry projections suggest:

Q2 2026: SSD prices may increase approximately 5–10% as enterprise demand remains strong and supply expansion remains cautious.

Q3 2026: pricing may stabilize with 0–5% growth, depending largely on inventory levels and hyperscale data-center procurement cycles.

DRAM Price Outlook

In the DRAM market, the ongoing transition from DDR4 to DDR5 continues to influence pricing dynamics.

Short-term projections indicate:

DDR4: price volatility may remain relatively high, fluctuating roughly within −5% to +10%, depending on specific capacities and supply adjustments.

DDR5: prices are expected to remain on an upward trajectory, increasing approximately 5–10%, supported by strong demand from servers and new PC platforms.

Overall, the structural shift toward DDR5 and the rapid growth of AI infrastructure are expected to continue supporting memory demand across both DRAM and NAND markets.

Procurement Strategies for Price-Sensitive Buyers

Given the current market environment, companies can adopt different procurement strategies depending on their inventory cycles.

Scenario A: Inventory Below 4 Weeks

For companies with short inventory cycles:

Implement phased purchasing plans

Increase inventory levels to cope with soaring procurement costs and the risk of stockouts for at least the next 2-3 months.

Prioritize locking prices for core capacities such as 512GB / 1TB SSDs and 16GB memory modules

This approach reduces exposure to short-term price fluctuations.

Scenario B: Inventory Above 8 Weeks

For companies holding larger inventories:

This strategy helps prevent overstocking during periods of gradual price increases.

Scenario C: Long-Term Project Customers

For long-term system integrators or enterprise projects:

If funds are sufficient, continue placing new orders to ensure that inventory remains available for sale in future cycles.

Establish forecast-based purchase orders

Long-term planning helps ensure supply stability and cost predictability.

KingSpec Supply Strategy

In addition to monitoring market trends, reliable supply chain management plays an important role in navigating memory price cycles.

As a professional storage manufacturer, KingSpec maintains a diversified sourcing and production strategy designed to reduce supply risks.

Key operational strengths include:

Diversified NAND sourcing channels

Stable monthly production capacity

Flexible lead times within 2–4 weeks

Multi-tier inventory buffer systems

Through this diversified supply chain structure, KingSpec is able to mitigate short-term spot market volatility of approximately 3–5%, helping customers maintain stable procurement plans even during fluctuating market conditions.

Conclusion

In summary, the global memory market in early 2026 is entering a phase of gradual recovery. Supply discipline from major manufacturers, increasing enterprise demand, and structural transitions toward new technologies are all shaping current price trends.

While moderate price increases are expected for NAND and DDR products through mid-2026, the overall market environment remains relatively stable compared with previous cycles.

For companies planning storage procurement or system upgrades, monitoring inventory cycles, enterprise demand, and technology transitions will remain essential.

As a professional SSD manufacturer, KingSpec provides reliable storage solutions supported by a flexible supply chain and stable production capabilities. If you are looking for dependable SSD supply for consumer electronics, industrial systems, or enterprise applications, contact KingSpec to explore our full range of SSD solutions and long-term supply support.